Table of Contents

Most sponsors lure prospective investors through sleek marketing materials and the promise of high returns. This may be a way to hook people, but as they say, the devil is in the details. Behind each offering, there is often a breadth of material that outlines crucial important information.

Potential investors should read these documents carefully to ensure they understand the risks associated with each deal. This is an essential part of any high net worth investor’s due diligence process.

In this article, we take a deep dive into one of those documents: the private placement memorandum (PPM). The PPM is where potential investors will learn about the nuances of the deal, the capabilities of the ownership team, the sponsor’s experience, financial statements and more.

What is a PPM?

A private placement memorandum, often times referred to as a PPM, is a document used in the context of a private securities offering. PPMs are relevant to real estate when a sponsor is raising capital for a syndication. The shares of which are sold as securities in that deal.

PPMs are a quasi-legal, quasi-business risk mitigation tool. The PPM describes the offering, the sponsor’s business plan, the risks involved, provides financial statements, and more. The document lays out all pertinent information that would cause someone to invest (or not) in a real estate syndication. This is regardless of a potential investors’ net worth.

People may refer to a PPM as a “Confidential Offering Memorandum” or “Confidential Information Memorandum”.

A private placement memorandum,

generally referred to as a PPM, is a document used

in the context of a private securities offering.

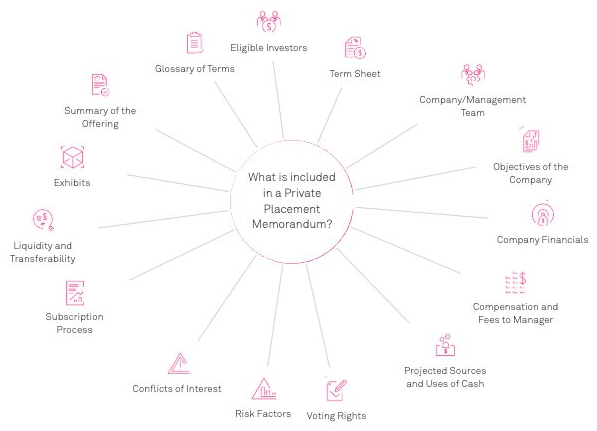

What is included in a Private Placement Memorandum?

PPMs are rather robust documents. They will often be 50-100 pages long. Here is an overview of a PPM, or the “anatomy” of a PPM:

Glossary of Terms

Glossary of Terms

It’s common for a PPM to include a glossary at the beginning. This helps eliminate any misunderstanding around what certain terms mean. Especially since so many acronyms and abbreviations are used in commercial real estate.

For example, the glossary of a Private Placement Memorandum might describe what it means to be an “accredited investor”. Which is especially important if that’s a requirement to invest.

The glossary may also define the Project, Property, Prospective Investors, Sponsor, and Units.

Summary of the Offering

Summary of the Offering

The summary provides a quick reference for those looking for specific information. For example, it might state that the Sponsor is seeking to raise XYZ capital in order to buy the “Property” (which will have been defined in the glossary already). It will state how many shares are being offered, for what price, and the minimum number of shares that must be purchased to invest.

The summary of the offering will also include brief snippets of the more detailed sections outlined below.

Eligible Investors

Eligible Investors

This section details who is eligible to invest in the deal. Some deals are open to non-accredited investors. Others are only open to accredited investors. The PPM may include a questionnaire to help investors determine whether they qualify as an accredited investor.

Note: to qualify as an accredited investor. The potential investors must earn $200,000 annually ($300,000 with a spouse) or have a net worth that exceeds $1,000,000.

This section of the private placement memorandum will also indicate whether the investment is IRA eligible.

Term Sheet

Term Sheet

The term sheet lays out the basic details of a deal’s financials. This is where, for example, a sponsor would indicate how much someone has to invest to obtain a certain percent ownership in the deal.

For example, the term sheet might say that a person is buying 85 shares of 123 Main Street LLC for $10,000 each. This equates to an $850,000 investment in the company.

The term sheet will also include basic information. This information could be the going in and expected exit cap rates, the hold period, and any preferred return someone might get as a Class A shareholder. Sample financial statements may also be shown here.

Company / Management Team

Company / Management Team

The sponsor has the most significant influence on the outcome of a real estate deal. This section of the PPM will talk about the sponsor’s management team. It will describe how the company is structured, who is in charge, the experience of that team and more.

This section will also include any key third parties that are crucial to the deal. Such as who the sponsor is using for legal, architecture, construction, property management, leasing, etc.

If any key player on the management team has a blemish on their track record, real estate related or otherwise, this is where that might be disclosed. The purpose of the PPM is to provide all relevant information that may influence whether someone invests in a deal.

Objectives of the Company

Objectives of the Company

This section of the PPM essentially describes the sponsor’s business plan. For example, the sponsor might be in the business of acquiring value add multifamily assets in the midwest that it intends to redevelop into Class B+ properties.

The objectives of the company may differ depending on whether the sponsor is raising money for a fund or a specific deal. If raising money for a fund, the objectives may be stated more broadly.

PPM describes the offering,

the sponsor’s business plan, the risks involved,

provides financial statements, and more.

This leaves the sponsor with some flexibility as they pursue new deals. If raising money for a specific deal, the “Objectives of the Company” may refer to the specific LLC being used for that deal. In situations like these, the LLC formed for that deal is the “company” and the sponsor will be more explicit about the LLC’s objectives as they pertain to that deal.

Company Financials

Company Financials

The sponsor should always include basic financial statements from their company. This could be the financial statements for the real estate investment firm or for the LLC formed for this specific deal.

At a minimum, the sponsor should include a profit and loss statement and copy of the company’s balance sheet (historical and forecasted). This shows prospective investors what kind of financial shape the company is in.

Compensation and Fees to Manager

Compensation and Fees to Manager

It is extremely important to determine how the sponsor will receive payment. This section of the PPM details the fees that a sponsor intends to collect. This may include an annual management fee equal to a certain %; an acquisition fee, and a preferred return after achieving a certain hurdle rate.

Projected Sources and Uses of Cash

Projected Sources and Uses of Cash

Every Private Placement Memorandum will often discuss the entire deal structure, equity and debt included. It will outline how much debt the sponsor plans to put on the property, where that debt is coming from (a traditional lender, etc.), and at what terms. It will also talk about the equity being invested. This includes both GP and LP capital.

The “use of proceeds” section will describe how the sponsor tends to spend that money. Let’s say a sponsor is raising $5 million in equity for a $10 million acquisition. This section will describe how the sponsor intends to use the LP’s capital to execute their business plan accordingly. Most sponsors will allow for some flexibility with use of proceeds to accommodate for inevitable project unknowns.

Voting Rights

Voting Rights

In most syndications, the LP investors will have very little authority over the direction of the deal. Sometimes LPs receive the right to vote under specific conditions. This section of the PPM will outline the circumstances under which a body of members can call a vote. For example, if the sponsor commits fraud, the members may choose to remove them as the GP.

The PPM will also indicate whether votes are tallied on a per investor basis or on a pro rata by ownership basis. It also specifies the minimum required vote precentage for success. Sometimes it will be a majority. In other cases, it may require a supermajority (“supermajority” will also be defined in this section of the PPM).

Risk Factors

Risk Factors

Some sponsors use an “off the shelf” PPM that includes generic risk factors. For example, it might state that past performance is not indicative of future performance. It might state that a downturn in the economy could adversely impact the deal and its returns.

Sophisticated sponsors will often work with their attorneys to customize the risk factors specific to each offering. The risks may be categorized, for instance, risks related to commercial real estate investment (broadly) or this company (broadly) vs. risks associated with a specific deal.

The risk factors are critical. They must be clear and thoroughly described. This section of the PPM is perhaps the most critical section of the entire PPM. Potential investors should focus closely on this section during their due diligence process.

Conflicts of Interest

Conflicts of Interest

This section of the PPM will outline any real or perceived conflicts of interest relevant to the company, its management, or the offering. For example, someone on the sponsor’s team may be a licensed debt broker and might be taking a commission for arranging the financing. The owner of the competing property down the street might also hire the same third party property management company.

In most cases, the conflicts of interest are relatively benign. However, the sponsor should still disclose these conflicts to investors in advance.

Subscription Process

Subscription Process

The PPM will also outline what potential investors need to do to subscribe to the offering. How much money must they invest, when, and what paperwork is necessary to do so? This may vary depending on an investor’s net worth and whether they are an accredited investor.

Liquidity and Transferability

Liquidity and Transferability

In most cases, syndication of real estate securities prohibits liquidation or transfer of them. However, some sponsors realize that individual investors may face unique circumstances that require them to sell their shares. This section of the PPM outlines the conditions under which those securities can be sold or transferred. It will also note whether investors will face a penalty for liquidating before the end of the hold period.

Exhibits

Exhibits

Most PPMs will include a series of exhibits. These may include the certificate of formation of the company, the company by laws or operating agreement (if an LLC), collateral about the business, press releases, and more.

What’s the difference between Public vs. Private Securities Offerings?

In a public securities offering, such as an IPO, a company must first register those securities with the Securities and Exchange Commission (SEC) or must pursue an exemption from doing so. This is a time consuming and burdensome process, especially for someone who is just raising a hundred thousand dollars (or even a few million dollars). That’s why most sponsors offer private securities. This skirts the need to register the securities with the SEC.

State and federal governing bodies would review all documentation if it was a public offering. In lieu of going through that process, a real estate sponsor may issue a PPM that provides all details for prospective investors to review on their own.

Why is a PPM Necessary?

The law does not actually require a PPM. Whether a sponsor uses one or not often depends on how much money they’re raising and from whom. For context, a PPM may cost $15,000 for an attorney to draft. If someone is only raising $100,000 from close friends and family, it may not warrant the cost of creating a PPM.

Most PPMs are authored by attorneys on behalf

of the sponsor and should be reviewed by the

LPs’ attorneys prior to investing.

As the size of deals becomes larger, and as sponsors begin to solicit investments from outside their immediate circle, the use of a PPM is often considered best practice.

Why is a PPM is so important?

If a deal goes wrong, the PPM often serves as a reference in legal disputes between the sponsor and the limited partners. For example, let’s say a sponsor is planning to redevelop a gas station. During the development process, the sponsor finds contaminated groundwater that will be expensive to remediate.

Assuming the PPM cites this as a risk, an investor would have a difficult time coming after the sponsor for project cost overruns. The risk was clearly laid out in advance and made known to potential investors ahead of investment.

Most sponsors have their PPMs written by lawyers and LPs should have their attorneys review it before investing. Reading the entire PPM is considered best practice for high net worth individuals conducting due diligence on deals.

In short, the PPM protects all parties involved in the transaction.

Conclusion

PPMs are robust documents that contain a breadth of information. For that reason, some potential investors merely skim through the documents. Sometimes they don’t read the PPM at all. They’re making a major mistake. The PPM contains vital information that all prospective investors should understand prior to making a capital commitment.

If you’re interested in learning more about PPMs, contact us today. We would be happy to share an example PPM from one of our prior offerings. We can walk through this example to help you become familiar with the PPM ahead of making your next investment.

FAQs

What is a PPM and when is it used?

A PPM is the core document for a private securities offering. In real estate syndications, it lays out the deal, the sponsor’s plan and team, the risks, and supporting financials so investors can decide whether to participate.

What does a typical PPM include?

Expect sections like a glossary of terms, a summary of the offering, eligible investor criteria, a term sheet, details on the company/management, objectives, financials, fee disclosures, sources and uses, voting rights, risk factors, conflicts of interest, exhibits, and more.

Is a PPM legally required?

Not always. Whether a sponsor uses one depends on how much they’re raising and from whom. That said, PPMs are often prepared by counsel and reviewed by investors’ attorneys because they become a key reference if disputes arise.

Who can invest, and how do “accredited investor” rules show up?

The PPM spells out eligibility. Some offerings allow non accredited investors; others don’t. It usually includes an accreditation questionnaire and the SEC income/net worth thresholds so investors can self verify.

What should I focus on when reviewing a PPM?

Zero in on fee structures, projected sources and uses of cash, voting rights, and especially the risk factors tailored to the specific deal. These sections drive economics, control, and downside understanding.

How do private offerings differ from public ones, and what about transfers?

Public offerings register with the SEC; private offerings generally rely on exemptions and provide disclosure via the PPM. The PPM also explains the subscription process and usually limits liquidity and transferability, with any allowed exceptions spelled out.